Investing 104: HOW to buy stocks - Dollar Cost Average

Dollar Cost Averaging is Cheat Code for Investing

I will use ‘DCA’ and ‘Dollar Cost Average’ interchangeably throughout the article.

Inspiration:

I did not read about DCA in a book or an article or a YouTube/TikTok video, I discovered it. While there is enough and more literature on dollar cost averaging, mine is a 100% original take on it. The initial spark, however may have come from Of Dollars And Data.

In his article titled “Just Keep Buying”, Nick Maggiulli makes a case for why you should just keep putting money to work, regardless of a bull or bear market.

I am excruciatingly honest, I did not read this article or his subsequent book on the same topic but heard enough about it on podcasts to have understood the gist. This, therefore, may have inspired my experiment into dollar cost averaging.

I think dollar cost averaging is a superior form of investing for retail investors. Even professionals dollar cost average but they do it in tranches or batches instead of buying small amounts everyday. If you are a more skilled investor, then you too could consider investing in a few large batches instead of small investments everyday.

Be honest with yourself though, how skilled are you really?

The Most Important Thing About DCA:

The most important thing about dollar cost averaging into a stock is that you better be right about the stocks you pick, be willing to change your mind when the facts change and ruthlessly follow the rules of entry, exit and rebalancing (Pro tip: Use limit orders for rebalancing and exits).

Up 20%, Down 80%:

How many times has it happened that you buy a stock and immediately after you buy it, it starts going down? It’s happened to me a lot and I’ll explain why later in the article. But like most problems I come across, I found a solution for this one too. You know what it is.

Add Risk Slowly:

Dollar Cost Averaging slows down the speed at which you take risk, gives you more time to process what you are buying and why you are buying. It allows time for you to reconsider your bullish/bearish stance, it allows for more news to hit for the narrative of the stock to move forward, more time for you to listen to what more bulls and bears have to say about any given stock.

DCA is Lazy!

DCA is also the laziest form of investing (Side Note: DCA with ETFs is straight up Garfield level).

DCA is lazy because you put in the work to build your conviction and then once you have conviction, you just keep buying, no matter what. As long as the thesis is intact, you keep buying until you hit your target allocation. (Pro Tip: I use the recurring buy feature to build these positions, so even if I am out traveling, I am kind of “actively” investing everyday).

The Technical Advantage:

I know a lot of people think Technical Analysis is Voodoo but it is not and I will write an article on it in the future.

Another benefit of DCA is that it breaks down technicals. Your entry/exit price, which otherwise would have been where the majority of the buyers’ entry/exit price is, because of dollar cost averaging, will have moved out of those technical areas of support and resistance.

For example, a stock made a high at $100, 2 years ago. You bought the top with everyone else. The stock falls and is at $50 now. The technical resistance for that stock is likely to be around $100, which literally means that a lot of people who bought it at $100 are underwater and waiting to liquidate and get out of this mess that they got into two years ago. Retail investors are terrible at taking losses (including me). So if and when the stock does come back to $100, it will face some selling pressure as it gets closer to $100. It could absorb that selling pressure and move higher but it is likely to experience some selling pressure, unless it’s doing something like Nvidia is doing these days.

But if you dollar cost average for 2 years, and the stock stays below $100 during that period, your average buy price, mathematically, is going to be below $100. How much lower depends on 1. How much you put in at the top at $100, 2. How much you chose to invest on a recurring basis, 3. How often you chose to invest on a recurring basis & 4. For how long?

So if and when the stock starts rallying again and gets closer to $100, you will either get an 1. An Early Exit: If you were holding a mistake that you could not take the loss on or 2. An Early Rebalance: If you think the thesis is still intact and the DCA was just to bring down your average buy price.

The trick is that you get your cash out at break-even before everyone else does. How much of an advantage you generate depends a lot on how aggressively you dollar cost average. And for you to do that aggressively on a stock which is down say 70% (as Rocket Lab was at one point), you need conviction, like absolute, rock solid, conviction. Borrowed Conviction Rarely Works.

Blood On The Streets:

Dollar Cost Averaging also makes it very very easy to buy on extremely red days. Days when my portfolio is down 15-16%, no kidding, I am sitting calmly, dollar cost averaging, so happy that I get to buy it cheaper today than what I was paying for it yesterday, and making memes about staying calm and dollar cost averaging.

These days which give you the best ROI, and are the hardest to buy on. But dollar cost averaging, by design, throws that out of the window.

WealthWise works on a very simple principle: Dollar Cost Average > Rebalance > Repeat. In terms of actions in the market (not taking into account my research and news publication), just specifically the actual act of trading in the market, these 3 steps encompass everything I do in the markets.

Dollar Cost Averaging is so central to my investing strategy that all my socials have “DCA” in them. As I said, it is the cheat code, so let’s dive in.

Why I DCA:

When I first started investing, like for most retail investors, I was tired of buying things and then watching them roll over just after I buy them. I would buy something because I read something somewhere or I heard some analyst somewhere and the stock goes up for a week, 1 month. I am up 50% on my position and then it all comes crashing down and I am bagholding with 30% losses.

This is why it happens: The fact that you, a retail investor, are hearing about a stock, that very act is what creates a top in a stock. By the time retail investors are talking about a stock, because they all got a tip from someone, the easy money has already been made. At this point a rush of retail money comes into the stock, Wall Street firms are always looking out for opportunities like this, so they push the price higher still, bringing in even more retail, eventually creating a bubble leading to the aptly named rug pull. The stock loses momentum and comes back down. (This doesn't always happen but happens a lot).

Dollar Cost Average is a very low effort way to solve this issue. Once I started Dollar Cost Averaging, it didn’t matter what price I started buying a stock at. What price to enter is not relevant anymore. Only thing that matters is that I pick good stocks. And let the market decide my buy price (See: You Are The Market Section).

The entry price is almost irrelevant. I say almost because how much you invest and how long you plan to dollar cost average to get to your target, matters a lot. If you want to do it in a month, then the entry price matters a lot, if you plan to do it over say 5 years, then it is almost irrelevant, simply because you give yourself more time to dilute your buy price by making smaller buys over a longer timeframe.

Having said that, you will definitely do better if you start buying at a good price and I will talk about it more in my future Technical Analysis article. But just by using a simple, lazy, powerful, trick like dollar cost averaging, you can reduce your entry price risk and increase your chances of generating alpha.

You Are The Market:

This realization did not happen until after a couple of years after I started dollar cost averaging across my portfolio. If you use Dollar Cost Average religiously for ~10 months, your average buy price is going to be the same as the 200 day moving average of the stock.

The 200 day moving average (DMA) is widely considered as an indicator that tells us where the stock is going in the medium term. Some people go so far as to say that just buy any stock that is above 200 DMA and you’ll be golden. And upwards trending 200 DMA is also considered to be bullish in the medium term.

Now, if you go ape shit on dollar cost averaging and double down on bad days, then your average buy price will be below the 200 DMA, again, just math. Generally, if your buy price is below the 200-day moving average (DMA), it is not considered a good thing as it often indicates a stock is in a downtrend and could be a sign of potential weakness in the long term, suggesting that the stock might be experiencing bearish momentum and could continue to decline in price.

But here it is happening just by design. If you buy the same amount of something everyday for 200 days and then buy a little bit more on days that it goes down more than normal, then your average buy price is going to be below the 200 DMA. So for that reason I don’t consider it alarming that you’re technically buying below the 200 DMA.

Now for the big reveal. If you have picked the right stock , and all this smart money is going to buy the stock once it is above the 200 DMA, and you got in say 10-20% below that because of being lazy and Dollar Cost Averaging, you are about to be rich. Once this flood of big money starts coming into the stock, it’s almost time for you to start taking profit. And that is why, You Are The Market.

How Tesla helped me “discover” Dollar Cost Averaging:

My first Tesla buy was on March 16th, 2017 - Price $262.40 (Pre-split) - Post split equivalent $17.49.

I built my descent Tesla position overtime. However, unlike today, where I invest with decades long time frame, back then I was just trying to make a quick buck. Just buying things I thought would go up with the intention to sell as soon as it went up a little bit. I did not have the experience I have today, nor the skillset.

Thanks to some appreciation in the stock price, Tesla soon became my largest position.

2018 was the time when Elon Musk’s colorful personality was just beginning to damage his reputation (the pedo comment was June 2018, 420 Tesla tweet was August 2018), you get the drift, the drama was just getting started. I acknowledge that it is way worse now.

In March 2020 though, shit hit the fan with Covid and Musk was behaving…kinda how he behaves now, but this was new back then. (I started writing this article long before the most recent outburst by Musk. What he is doing is now is New New)

So on a little push from a friend (who I don’t blame - because YOU are alway responsible for the trades you make), I started selling my $TSLA position and booked some profit. As mentioned earlier, I was speculating and had never made 100% on a stock in my life, so I really had to make sure I got that sweet sweet Mooooney!!!

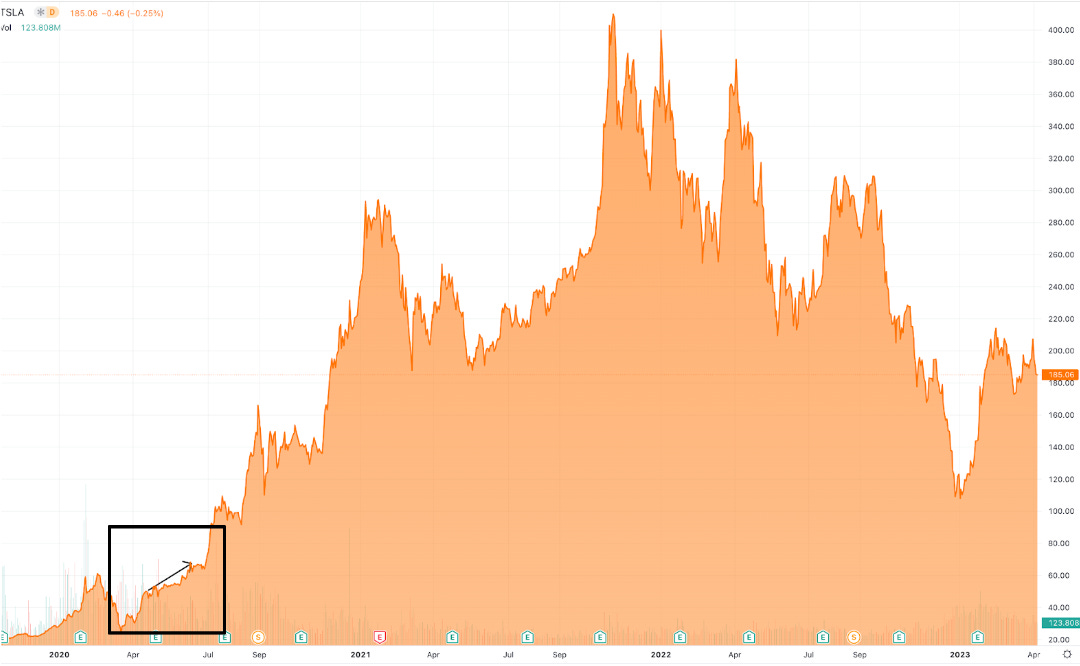

After struggling with Elon’s antics for a while, finally, on April 21st 2020, I put in my final limit order and it went through at $696.05 (Pre-split) - Post split equivalent $46.4 (Bottom of tiny arrow in Tesla graph below after the screenshot (bottom left))

My $TSLA thesis was unchanged (still hasn’t), I just sold it because I made a lot of money and didn’t want to not cash in. I was greedy and lacked patience and maybe even lacked some conviction (nothing like I have today). So, I was still bullish on Tesla and wanted to be part of the story. I always thought of Tesla as one of my top 3 investments. So, I needed to get back in.

By June 11, 2020, $TSLA had gone up above $1000 and come back down.

I was desperate to get back into Tesla. But Tesla still looked expensive, experts on Wall Street were saying it would come back down to $100. There was so much fear, uncertainty & doubt in the market that I was convinced $TSLA would come down to $300. [Top of tiny arrow in Tesla graph above (bottom left)]

I thought Tesla’s fair value then was $300 (pre-splits), but Tesla was trading close to $800. So, I made up my mind to buy 1 stock and get some “skin in the game”. My goal at that time was to eventually buy 10-12 stocks, basically a $10K position. So, I’m putting in 8% of my total investment that I intend to put in today. However, at that moment, I didn't do all this math, I was just desperate to get in and didn’t have the patience to wait.

And I am so glad I did, because you can see in the chart what happened to the Tesla Stock Price post June 11th, 2020 [From the top of tiny arrow on the graph above to ~$250 where Tesla closed last week).

On August 11th, 2020 Tesla announced a 5:1 stock split and the stock didn’t look back from there, it went supersonic. With just that 1 stock, Tesla grew into my largest position (minus Google at that time).

That is when I realized that Dollar Cost Average is a win-win. If the stock goes down, good, you still gotta buy more, so you can continue to buy cheaper. And if it goes up, then no reason to complain, you made some money. Cheat code.

Anyway, coming back to Tesla, the stock was back in the dumpster in 2022. And guess what the ‘investor’, not the ‘speculative trader’ do? I dollar cost averaged into my buy, Buying 1 stock for every dollar drop in price. I managed to get my lowest buy at $102 on Jan 6th, 2023. The 52 week low was 101.81.

I remember a friend asking me: When will Tesla bottom? I told him, I don’t know and I don’t care. I have limit orders in place and they keep building my position, as the stock price keeps going down. I honestly don't know if I would have had the courage to buy it on those days when it was a falling knife if I did not have this rules based system.

I am now at 100% allocation on Tesla with an average buy price of $155.11 and have also recently started taking profits in Tesla as it is above 5% of my net worth allocation target. I recently posted a trade alert with details of this trade which is for paid subscribers only.

Disadvantage of Dollar Cost Averaging?

One can argue that the biggest disadvantage of Dollar Cost Averaging is that sometimes you will miss the train.

I agree, and I have some examples like that. But Dollar Cost Averaging made me more patient, most of those stocks that run away from me, often come back down and I end up buying them cheaper instead of chasing them. Some never come back and for those, you have to keep your ears on the ground everyday - one great way to do just that is Alpha Coverage, built for people who want to learn but don’t have the time, at least that is what they say.

Unless you are willing to put in that kind of work, you won’t catch the Nvidia’s of the world in time and are likely to miss it regardless of whether you are Dollar Cost Averaging or not. In fact your miss rate would likely be higher if you were not dollar cost averaging by account of having entered a stock with a bulk investment at the wrong time and having zero investments in some of the winners (vs. having a tiny amount).

Rocket Lab:

I started buying Rocket Lab at $11.78, my current average buy price is $5.16. That’s more than 50% lower. I can hold more than twice as much Rocket Lab stock for the same amount of money. That is the power of Dollar Cost averaging.

Timing the Market:

The hardest thing to do in the market is timing, because you have to do it twice, on the way in and on the way out and if you miss either, it does not work. And contrary to popular belief, getting back in is way harder because when markets move, they won’t give you a chance to get back in.

With dollar cost averaging, it is a slow drip in, you just keep building a position over time and that leaves you with having to time the market only once, when you are exiting a position.

Staggered Buys:

I also want to take a moment and talk about buying in batches instead of buying all at once or dollar cost averaging. Professionals often use this strategy, where they will buy 25-50% of their intended position first and then make a couple of more buys to complete their position. I am not opposed to this strategy. I have used this strategy often including Nvidia, Tesla and more recently Vistra & Constellation Energy to help me get to my desired position quickly as I could see bull market taking these stocks higher.

Buying in Bulk:

I don’t recommend putting all your money in at once, no matter how much of an expert you are. I’ve learned over time that very few people are really experts and even they can’t always tell where the stock price is going in the short term.If you have a lot of money to put to work, then maybe go for staggered buys and then transition into dollar cost averaging. You don’t want to be sitting with a pile of cash for too long though. Depending on when you want to deploy that cash, you should invest 80-90% of it within 3 months, especially if you get this money in August. Seasonally, mid-Aug to mid-Oct the markets are lower. I usually make big changes to my portfolio between August and October each year.

My Dollar Cost Average Process:

Fundamentals: Do your due diligence and know what you are buying, why you are buying it and for what time frame. My next Edu article is likely to cover the subject of WHAT to buy.

Bank Balance: Make sure you have enough cash to support the strategy. Figure out how many stocks you want to buy, how often and how much, do the math, to make sure you have the cash flow to sustain the strategy. I’d strongly recommend starting with a small number, it grows on you very fast. I ended up using a six figure number to feed my strategy over the last 4 years, which I had not anticipated.

Discipline: Be disciplined and follow the strategy religiously, if you don’t end up buying in the 10 days when the market was bottoming, when you were scared, then that will take away a large chunk of your alpha. In the same way, rebalance when you hit your targets to keep the excess cash flowing and feeding the system.

When to Cut & Run: Sell when you lose faith: There is no point holding on to a stock or to dollar cost average into it if you lose faith in its ability to grow equity. Once the thesis is lost, get out! Take the loss. Tax loss harvest.

Target Allocation: When you dollar cost average, you also need to set a target allocation. How much money do you want to put in? I have 4 different allocation targets. I allocate all my positions in one of these 4 targets: $1K, $2K, $5K and $10K based on how bullish you are on any given stock.

Rebalance any excess principal invested above your allocation target, at or above your breakeven price to raise cash to keep feeding the DCA beast and make sure you are not over exposed in that stock.

Switch “Allocation Target” from “Principal Invested” to “Equity”

Since my intention is to make money and not only rebalance at break-even; During bull markets, instead of looking at my “Principal Invested” as my “Allocation Target” (so the $1k to $10K investments), I shift my focus to my entire “equity” in any given stock (and not just the principal).

Allocation Target is retired and it becomes “Rebalancing Target”, for which instead of looking at how much money I invested (Principal Invested), I look at a percentage of my net worth. For example, it could be 5% or 2% of my net worth depending on my conviction for any given stock.

So instead of rebalancing at breakeven, I wait for the stock to climb to 5% of my net worth and I then start re-balancing. In the most recent times, I have been rebalancing $NVDA $TSLA & $AAPL using this strategy.

You could almost make a rule of thumb to more aggressively rebalance around a “Principal Invested” target during a bear market and switch to a more growth friendly “Rebalancing Target” by focusing on the current equity in the stock, during a bull market.

For example, Nvidia grew 600% before it reached my 5% of net worth target, when I started rebalancing it. Making the switch in the bull market, gives your investments space to grow.

Changing Allocation Target: If you like a stock a lot, you could consider raising your allocation targets at both the principal invested level as well as the total equity level.

This is not something you do very often, like less than 5 times in your entire life.

Take into consideration your near term liquidity needs, where the market is trading, multiple and growth prospects of the stock you are holding.

I’ve only done this once so far, when I increased the Rebalancing Target for RocketLab from 5% of my net worth to 10% of my net worth.

Liquidate Entire Position: If you are not particularly bullish on a business going forward, you could also liquidate an entire position. This is critical to do when dollar cost averaging or else you will end up buying the stock into oblivion.

Dollar Cost Average > Rebalance > Repeat.

Example:

Say you set a target allocation on a principal invested basis for a stock $XYZ at $5k. You made this purchase 2 years ago and in the last 2 years, the stock has been in a trading range. So your $5K has swelled to $7K and also down to $4K.

Given that we are in a trading range and not in a bull market, we will rebalanced based on ‘Principal Invested’. So when it goes to $7K, you shave off $2K and still maintain your $5K exposure. And when stock $XYZ goes down by more than 10%, I start to add to it again. The reason why I pick 10% is that if I am going to rebalance based on ‘Principal Invested’ at breakeven, buying 10% down means I make 10% each time I rebalance at breakeven. I have set a goal of minimum 10% gain for any investment I am going to make.

Please take note these are often held for a few months, hence the annualized return is a lot higher.

Now when we break out of the trading range and you see your stock going higher, then in that case, I will switch my ‘Allocation Target’ to 5% of my net worth on an Equity basis.

So let’s say my net worth is $500K, which makes 5%, $25K. So if and when my $XYZ position gets to $25K, I will start rebalancing on a Equity basis anything above the $25K mark.

It is very important to note that this $25K number is not static and will change since the 5% is pegged to the net worth. As long as the net worth is growing, the actual dollar value for that the 5% represents will keep growing. This allows you to continuously take distribution from your stocks, at the same time, your overall allocation in actual dollar terms keeps growing. I have shared before that my Nvidia position is now 40% higher than when I first started taking profit.

Rebalancing is “The Prestige”

Rebalancing is the second most important skill one needs to master, to make money in the stock market. Hence it deserves a whole separate article.

Obviously I will write about the most important skill too! Or did I already do that? Subscribe to find out!

End Game

Once you are positioned, each time the market goes up, you get some cash when you rebalance and each time the market goes down, you put that same cash to work. With each up and down, you make some extra percentages on your portfolio, this will be above and beyond what your long term returns would have otherwise been, hence juicing up your returns and delivering that sweet sweet alpha.

I tend to make ~5-10% with each down-and-back-up swing of the market across my entire portfolio and closer to ~10-30% in my higher growth portfolios. For now, only one of these high growth strategies is publicly available and you can access it with a paid subscription:

Borrowed Conviction Rarely Works

Past performance is no guarantee of future results.

The ideas discussed in this article should not be constituted as investment advice.

I reserve the right to change my mind if the facts change.

Disclosure: We own positions in some/all of the tickers mentioned in this article.