$ENPH & $FSLR: Solar Powerhouses

Why I am doubling down on Solar

This is a follow up article to The Next Bull Market, where I made the case for Renewable Energy to lead the next bull market. While AI has captured our imagination at the moment, we are living through the hottest summer since we started keeping records and the UN recently announced that we are no longer in ‘Global Warming’ but are instead entering ‘Global Boiling’. It might very well be the case that climate change and global warming is one of the first problems that AI will help us solve.

Out of the stocks I wrote about in that article, TSLA, ENVX, SLDP & others have done well but not $ENPH. So let’s take a look at $ENPH and today I will add $FSLR to the list.

Q2, 2023 Earnings:

Enphase Energy reported earnings on July 27th, 2023 beating on EPS and a miss on revenue. The stock sold off in the after hours owing to lower revenue guidance for Q3, seeing sales of $555M-$600M, far below the $749M analyst consensus estimate.

First Solar also reported earnings on July 27th, 20923 beating on both top and bottom line. Guidance was in-line: Net Sales $3.4B to $3.6B vs $3.46B consensus; EPS $7.00 to $8.00 vs $7.24 consensus.

I previewed this outcome in Alpha Coverage 13, in the Editor’s Pick section, where Beth Kindig made the case in her article that $ENPH won’t benefit that much from the Inflation Reduction Act in the short term while $FSLR will. In the same newsletter, in the Editor’s Pick section, I also called out Susquehanna’s note on softer demand for $ENPH.

So where do these stocks go next?

Enphase Energy - ENPH 0.00%↑

For a refresher on what $ENPH does and why it is important, please refer to my previous article: The Next Bull Market. But why has Enphase Energy lagged?

Interest Rates:

The Federal Reserve has raised interest rates by about 550 basis points over the last ~1.5 years. This was expected to hit the interest rate sensitive areas the most. So, usually large purchases for which people or institutions borrow money. Expectations were that housing would take a big hit, people would pull back on large purchases like cars, home renovation, setting up solar, etc… Some of it happened and some of it did not.

While housing equities pulled back, real estate prices never actually crashed like the market was expecting. The most interest rate sensitive section of the market did not move much because 1. There is no supply. If there is no supply and the market remains tight, prices won’t fall. 2. Home owners are not selling because they have locked in 30 years of low interest rates and moving now would increase their monthly mortgage payment considerably. I also covered this in more detail in my article Real Estate Investment - Without the Baggage.

However, while interest rates did not hit real estate as the market was expecting, it did hit the other segments like cars and solar installations. This is the same reason Tesla had to give out such large discounts to stimulate the market and which is one of the reasons why Solar has slowed down in the last 6 months.

However, the Fed is either done or almost done hiking, which means demand will stabilize here. I also think the Fed will cut interest rates a little bit in H2 2024. Which will be a tailwind for interest rate sensitive sections of the market.

Impact of NEM 3.0:

NEM 3.0 is a new net metering policy for California that was passed by the California Public Utilities Commission (CPUC) on December 15, 2022. It was implemented on April 14, 2023.

NEM 3.0 reduces the value of exported energy by about 75%, which leaves rates at a fraction of what they were under NEM 2.0. It extends the solar payback period for customers who generate electricity with their renewable energy sources. This means it will take longer for homeowners to receive a positive return on their investment in solar energy.

Pairing solar with battery storage will be more beneficial under NEM 3.0, which is a silver lining in itself because $ENPH provides batteries too. Read more about the impact of NEM 3.0 here.

These are important issues that are plaguing Enphase’s growth in the short term but if you zoom out, the secular story of Energy Transition and specially solar’s role in it is intact and if you can look past the short terms negativity, you will see the stock has already priced in this bearishness.

Path Forward:

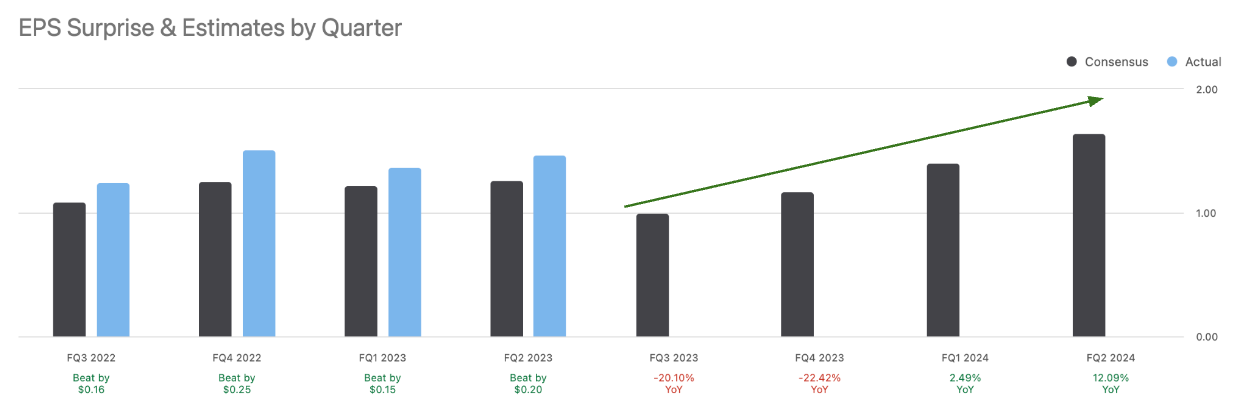

As you can see in the chart below, Earnings are expected to bottom in Q3, 2023. And Stocks usually look forward by 6-12 months. With the Fed done raising rates (almost), the economy rebounding, industrials rising and “global boiling” taking hold, dare I say are we at the bottom for $ENPH? If there was only a way to confirm!

Source: Seeking Alpha

Enter: Technicals:

Source: Robinhood

Technical analysis sounds like voodoo but trust me, it works, not always but as one data point in many, it is essential.

So what we see here is that on a 5 year chart, $ENPH is kissing its 200 day moving average (dma) - Blue Line. The 200 dma is often considered to be strong support and in most cases the stock should bounce off the 200 dma. However, it is possible that it breaks the 200 dma support, in which case, the stock should find some support at $120 where it bounced from in May 2021 & Jan 2022. Buyers seem to come in at that price.

Technically, the red line, the 50 dma was also support, until it was broken, so it is very possible that we break the 50 or 200 dma. Though I am betting ENPH 0.00%↑ does not break the 200 dma and bounces off of it.

Post earnings, the stock sold off but recovered half of it the following trading day. This is bullish: When stocks stop going down on bad news.

Valuation:

23 analysts on average suggest Enphase Energy will deliver earnings of $8.81 in 2025 which equates to a P/E of 17.52 at current prices (Source: Seeking Alpha). I think $ENPH is a steal here.

Positioning:

I have a full position in $ENPH. I will continue to dollar cost average and bring down my average buy pice and re-balance on the other side.

First Solar - FSLR 0.00%↑

First Solar stands to benefit the most from the Inflation Reduction Act as the IRA’s primary objective is to spur investments in US domestic manufacturing capacity. Here are excerpts from Beth Kindig’s Article (mentioned earlier): First Solar And Other Renewable Energy Stocks That Benefit From $400 Billion IRA Bill (I will strongly encourage you to read this article, if you have not already):

We believe those companies that have these three characteristics stand to benefit the most. 1) Meaningfully collect the IRA corporate tax credit 2) Established US based manufacturing operations and 3) Viewed as important players in the IRA.

Based on these criteria, we believe First Solar (NASDAQ:FSLR) stands to benefit. Furthermore, we believe that First Solar has positioned itself as one of the national champions in its implementation. In First Solar’s Q422 earnings call, they provided initial guidance as to the positive financial impact the credit would have in 2023.

We have a preference for companies who are selling to utilities such as First Solar rather than those selling to consumers via installers, such as Enphase. Enphase will not immediately benefit and the impact will be smaller, plus management pointed out near-term macro concerns due to higher interest rates affecting their business.

Corporations with US manufacturing capacity are the biggest beneficiaries with an estimated $216 billion worth of tax incentives available. They are meant to provide an incentive for private domestic investment in clean energy, transport and manufacturing.

One of the reasons First Solar stands out is due, in no part, to the fact that they have provided the most visibility as to how the IRA will impact their earnings. In doing so, they have provided a useful investment framework to assess how other companies may benefit. Not every company will see this type of impact on their profitability.

The impact on earnings is significant. Consensus earnings are expected to increase 80% from 2023 to 2024 and 50% from 2024 to 2025. Comparing it to 2022 is not an apples-to-apples comparison as there was no IRATC benefit in 2022 while gross margins were impacted by higher than expected logistic related costs. There were mainly penalty costs related to exceeding dock waiting times due to Covid supply-chain issues. FSLR has indicated that these and other costs will trend back down toward pre-pandemic levels over the course of the year.

FSLR manufactures solar modules based on thin film Cadmium Telluride (CadTel) photovoltaic (PV) technology demonstrated to have lower cost, superior scalability, and a higher theoretical efficiency limit over conventional technologies, like crystalline silicon (c-Si). Solar module sales represented 93% of total sales and the majority of sales were to developers and operators of systems in the United States. A few of its largest customers include Intersect Power, Lightsource BP, and NextEra Energy.

Valuation:

10 analysts on average suggest First Solar will deliver earnings of $20.07 in 2025 which equates to a P/E of 10.38 at current prices - (Source: Seeking Alpha)

First Solar has a Non-GAAP Fwd. PEG of 0.94.

Technicals:

First Solar looks good technically, asset prices trend and $FSLR is trending only one way - Up!

Positioning:

I am at 24% to target on principal and 41% on equity. I increased my position by 25% last week and am aggressively adding to $FSLR with the goal to get it to 100% asap.

Past performance is no guarantee of future results.

The ideas discussed in this article should not be constituted as investment advice.

Disclosure: We own positions in some/all of the tickers mentioned in this article.

Borrowed Conviction Rarely Works