Should I be buying Nvidia Right Now?

Keep Calm & Dollar Cost Averaging

On May 24th, Nvidia reported Q1, 2023 earnings and shocked the markets with a jaw dropping guidance which took the stock 25% higher in trading the following day.

Nvidia (NVDA) said it expects second-quarter revenue to be $11B, plus or minus 2%, well above the $7.18B analysts were expecting - That’s a ~53% beat on guidance.

The stock was up ~113% going into earnings, and went up another 25% the next day. The graphic-chip maker’s epic stock market jump was greater than the entire market capitalization of Wall Street titans Goldman Sachs or Blackstone Group (MarketWatch).

This move surprised everyone, just ask Cathie Wood!

Suddenly everyone comes to the realization that they are underinvested in Nvidia/AI, including yours truly. So what should we do, do we buy more, right now? Or do we wait for a bit? In this article I am going to make the case for why Nvidia is not as expensive as you think and share some strategies to increase exposure.

Valuation:

I’ll start with the elephant in the room, since that is what everyone seems to be worried about: Valuation.

“Before Nvidia reported it’s blockbuster earnings, Nvidia was trading at $305 and that was 67 times consensus earnings for this year, today, it’s trading at $380 and that is 53 times consensus current year earnings”

Paraphrased from Michael Santoli on CNBC

Please take note, that is a 21% multiple compression for THIS YEAR (for the rest of 2023), based on ONE earnings report. So keep that in mind when we talk about P/E & valuation.

AI is a multi-decade tailwind, so let’s not overreact simply because the stock went up a lot. Let's add some historical context to this and also look at projected numbers into the future.

Nvidia’s Has Always Been Expensive:

Source: Seeking Alpha (May 27th, 2023)

Nvidia has historically traded at a high multiple. High tech companies that are on the cutting edge are seldom cheap. While never cheap, Nvidia did trade at more reasonable valuations around early 2019 and December 2022, when looking at the last 5 years.

Source: Seeking Alpha (May 27th, 2023)

During the same 10 year NVDA has returned 10,593%, 527% in the last 5 years. The entire time, it was “expensive”. Just eyeballing the first chart, I can safely say that the average P/E for the last 5 years has been higher than 40-45.

Nvidia’s Forward Multiple:

“Nvidia’s next year’s earnings were expected to come in at 52 times before the earnings report, it’s now down to 42 times”

-Brad Gerstner made the point on CNBC’s Halftime Report

That’s bang in the middle of Nvidia’s last 5 year average P/E. So we could make a case that Nvidia is fairly valued, even after the 25% surge because the earnings expectations climbed significantly.

But that would be an incorrect statement because Nvidia is at the first step of a very long journey and Nvidia is The One-Stop AI Shop, Seeking Alpha author Ivana Delevska writes.

Nvidia’s Potential:

A Shift in Compute: CPUs to GPUs:

Nvidia believes it’s riding a distinct shift in how computers are built that could result in even more growth — parts for data centers could even become a $1 trillion market, Huang says.

Historically, the most important part in a computer or server had been the central processor, or the CPU. That market was dominated by Intel, with AMD as its chief rival.

With the advent of AI applications that require a lot of computing power, the GPU is taking center stage, and the most advanced systems are using as many as eight GPUs to one CPU. Nvidia currently dominates the market for AI GPUs.

“The data center of the past, which was largely CPUs for file retrieval, is going to be, in the future, generative data,” Huang said. “Instead of retrieving data, you’re going to retrieve some data, but you’ve got to generate most of the data using AI.”

“So instead of millions of CPUs, you’ll have a lot fewer CPUs, but they will be connected to millions of GPUs,” he continued.

Nvidia’s GPUs tend to be more expensive than many central processors. Intel’s most recent generation of Xeon CPUs can cost as much as $17,000 at list price. A single Nvidia H100 can sell for $40,000 on the secondary market.

Source: CNBC

The Software Angle:

Analysts say that Nvidia remains in the lead for AI chips because of its proprietary software that makes it easier to use all of the GPU hardware features for AI applications.

Huang said Wednesday that the company’s software would not be easy to replicate.

“You have to engineer all of the software and all of the libraries and all of the algorithms, integrate them into and optimize the frameworks, and optimize it for the architecture, not just one chip but the architecture of an entire data center,” he said on a call with analysts.

Source: CNBC

“We had the good wisdom to go put the whole company behind it,” CEO Jensen Huang told CNBC in an interview last month. “We saw early on, about a decade or so ago, that this way of doing software could change everything. And we changed the company from the bottom all the way to the top and sideways. Every chip that we made was focused on artificial intelligence.”

In 2006, the company made another huge bet, releasing a software toolkit called CUDA.

“For 10 years, Wall Street asked Nvidia, ‘Why are you making this investment? No one’s using it.’ And they valued it at $0 in our market cap,” said Bryan Catanzaro, vice president of applied deep learning research at Nvidia. He was one of the only employees working on AI when he joined Nvidia in 2008. Now, the company has thousands of staffers working in the space.

“It wasn’t until around 2016, 10 years after CUDA came out, that all of a sudden people understood this is a dramatically different way of writing computer programs,” Catanzaro said. “It has transformational speedups that then yield breakthrough results in artificial intelligence.”

Source: CNBC

The Heart:

Huang, 60, immigrated to the U.S. from Taiwan as a kid and studied engineering at Oregon State University and Stanford. In the early 1990s, Huang and fellow engineers Chris Malachowsky and Curtis Priem used to meet at a Denny’s and talk about dreams of enabling PCs with 3D graphics.

The trio launched Nvidia out of a condo in Fremont, California, in 1993. The name was inspired by NV for “next version” and Invidia, the Latin word for envy. They hoped to speed up computing so much that everyone would be green with envy — so they chose the envious green eye as the company logo.

Source: CNBC

As I have stressed on the importance of having great management teams in the past, “Inspiration” is critical for having great management teams. Which is why I included this snippet so we know the genesis of the idea and for how long they’ve been at it.

Yes there is exuberance but we are no where close to the 2000 tech bubble but it has started to happen.

At the March 2000 peak, Cisco’s price-to-earnings ratio stood at 201 times, its enterprise value to sales at 31 times and its price-to-free cash flow at 176 times.

Source: Financial Times

Leadership:

Gaming - Leader: Nvidia

Crypto - Leader: Nvidia

Metaverse - Leader: Nvidia

AI - Leader: Nvidia

See a trend? Nvidia has always been a leader in cutting edge chips, no matter the industry.

Growth:

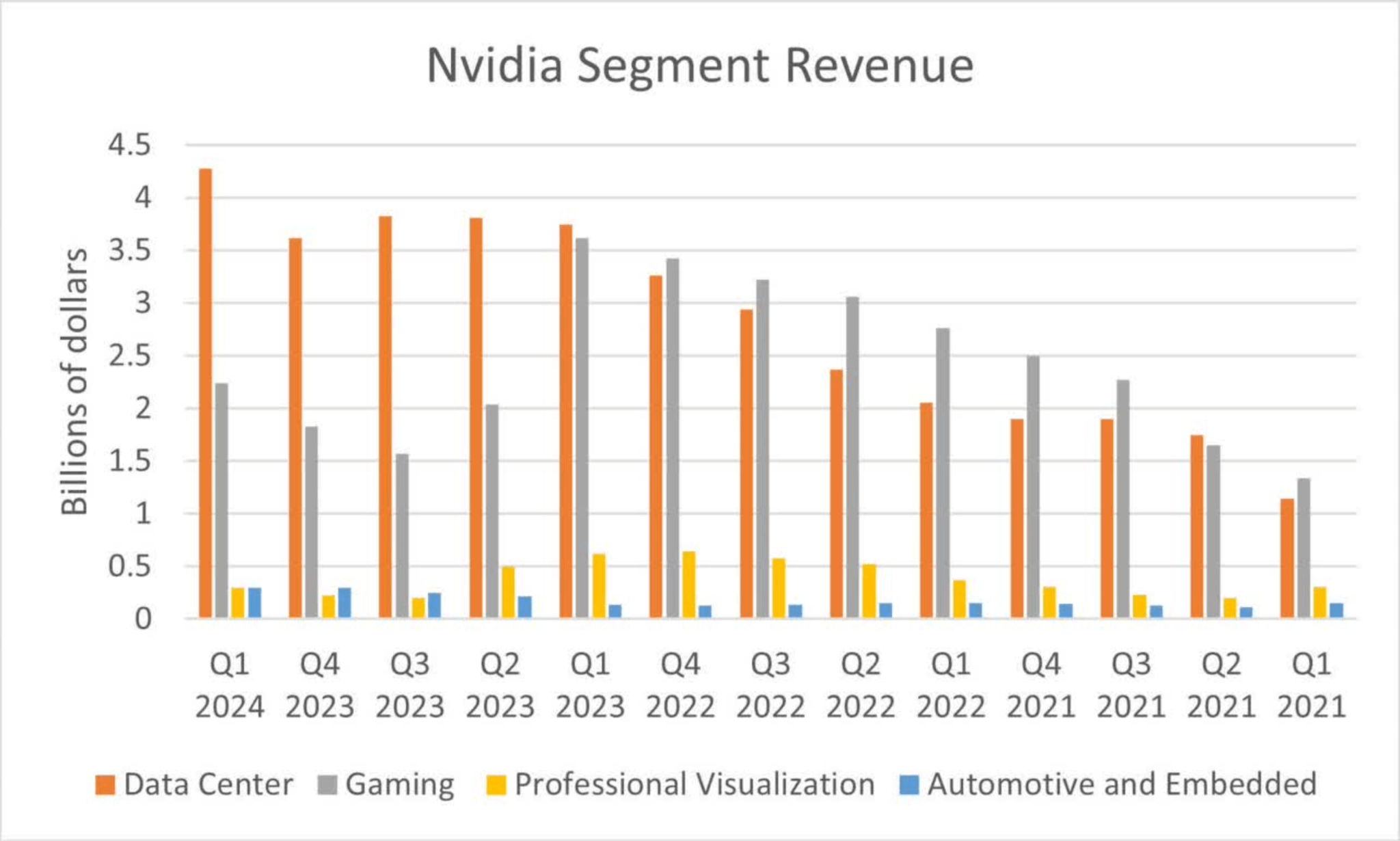

This focus of this article is to make a case for why Nvidia is not as egregiously overvalued as some believe, so I am not going deeper into Nvidia’s other business lines but here is a quick snapshot on growth trajectory across other business lines and brief commentary.

Source: Seeking Alpha

Data Center revenue has taken off on the back of AI.

Gaming has bottomed and has been growing QoQ in the last 2 Quarters. The gaming graph has the Crypto boom-bust cycle in it. In fact, we could be on the verge of a new Crypto boom cycle with digital authentication becoming more and more important. Here is a small clip from The Compound & Friends last week’s episode where they make the connection between AI & Crypto.

Professional Visualization which is basically the Metaverse and Nvidia calls their platform Omniverse. Nvidia’s Omniverse is focused on going beyond the Metaverse and into commercial applications and enterprise solutions.

Automotive platform ‘Drive’ is just getting heated up. I would say we are further along in AI than we are in automotive. AI is also necessary for Automotive to deliver, which is the sole focus of Tesla.

For a more in depth analysis of the various business segment, check out this article by Deep Tech Insights on Seeking Alpha where they make a case for $348 fair value for Nvidia.

Competition:

There is no doubt competition, after all this is the Holy Grail of tech.

Nvidia will face increased competition as the market for AI chips heats up. AMD has a competitive GPU business, especially in gaming, and Intel has its own line of GPUs as well. Startups are building new kinds of chips specifically for AI, and mobile-focused companies like Qualcomm and Apple keep pushing the technology so that one day it might be able to run in your pocket, not in a giant server farm. Google and Amazon are designing their own AI chips.

Source: CNBC

Apart from the names mentioned above, Tesla is also a significant competitor when it comes to AI Chips. Jim Breyer thinks Google is Nvidia’s biggest competitor.

Important to note that hyperscalers like Amazon, Microsoft & Google have a vested interest in developing these chip in-house given the high price point and potential that could have on their margins and bottom lines.

The ‘E’ In P/E:

Essentially what I am saying is don't make decisions based on legacy P/E numbers and take into consideration that the E in P/E could be wrong/could change. It could be higher or lower. What we have is just an “estimate” based on analyst projections.

As Joe Fahmy says in his tweet:

“The greatest winning stocks throughout history traded at 1.7 times the market's multiple BEFORE they made their big moves. Therefore, if you refuse to buy a higher PE stock, you've instantly eliminated the best potential stocks from your universe.”

My Nvidia Position?

I was in the trenches buying Nvidia when it dropped late last year and into January of this year, I got to 45% of my intended position. However, with the recent surge, my equity has grown to 110% of my allocation target (Principal is still at 45%). So, if I did want to re-balance, I could sell 10%, but because of the thesis I laid out above, I have instead been buying more Nvidia. I have doubled my target allocation and hence my current equity position is at 55% to target. It is very rare that I would increase a target allocation on a stock, maybe once a year or once in two years. So this is extremely rare. Usually I would stick to my target and re-balance but I am adjusting my allocation based on my net worth and prospects for the individual investment.

Should I Buy Now?

The secret sauce is Dollar Cost Averaging. I’ve mentioned before that I “discovered”' Dollar Cost Averaging, trying to get into TSLA in June 2020. I am following the same playbook now.

If you feel you are underinvested in Nvidia, start Dollar Cost Averaging a very tiny amount each day using recurring buys each day. I’d recommend this amount to be so tiny that you don’t notice it but if left untouched for a year, would lead to your intended position size.

If Nvidia stock pulls back, either increase the denominations of your recurring buy or make bulk buys. I like to use “Limit Orders” to build positions, so my orders go through even if I am not looking.

Over time, one of three things will happen

The stock pulls back, in which case you can easily build your position

The stock goes sideways, you will end up building your position over time

The stock could go up, you have some skin in the game and you make some money but you didn’t take the risk, so you didn’t get the huge pay off (if there is one down the road).

A more aggressive strategy would be to layer in your investment as a % of target allocation. In which case, I would start with:

10% if the stock is close to $400

25% if the stock is close to $350

50% if the stock pulls closer to $300

Then use the left over strategically to layer into the stock. This is what I would do if I didn’t have a position in Nvidia at all. I would keep a recurring buy to Dollar Cost Average throughout (even when I am buying % of allocation).

Nvidia Could & Will Likely Pull Back:

I think there is a good chance the stock could pull back. There are a lot of technical reasons like shorts covering and profit taking which is human nature. Stock has gone up a lot, let me take some off. I don’t blame anyone for taking profits. In fact, I encourage you to take profits and rebalance. It is healthy and a good sign of risk management. Don’t fall in love with a stock, it’s a means to an end. If you feel you are overexposed (have a large percentage of your net worth exposed to Nvidia), then you have to re-balance, no matter what the returns you are leaving on the table. It’s not as if you are selling all of it, that would be a mistake in my opinion.

So the stock could pull back in the next few days but I strongly believe it won’t stay there for too long as every dip will be bought. So if you decide to Dollar Cost Average, be ready to pounce - if and when you get this pull back.

There are a lot of other risks on the horizon beyond valuation, growth and competition. Taiwan/China remains a big risk and is the primary risk to the Nvidia story. The debt-ceiling is due to be signed this week. I don’t see high interest rates and receding inflation as being of particular risk, unless things take a turn for the worse. Nasdaq has been a bull market for a few days already and I am starting to see the new leadership emerge: Nvidia & Tesla.

Bottomline:

Nvidia is expensive, based on numbers we have access to today, no doubt! But when you walk into a store, you don’t pay the same price for everything, somethings are more expensive for a reason, and sometimes not! Your ability to identify the difference is what makes you a great investor. I think Nvidia’s MOAT & Leadership in Data Centers, Gaming, Professional Visualization & Drive & the growing importance of cutting edge chips as our lives become more and more digital, will lead to more growth for Nvidia.

If I don’t have exposure, I need skin in the game.

If I have exposure, I’ll hold.

If I am over exposed, I’ll book profit.

Subscribe to my weekly newsletter that brings you a summary of critical, thesis changing stock market news.

I write about topics like Renewable Energy, Companies Thriving In Space, Dividend ETFs like SCHD, Income ETFs like JEPI & JEPQ & REITs.

In this week's Alpha Coverage Newsletter, we shared a clip about how we could be underestimating the strength of AI.

Past performance is no guarantee of future results.

The ideas discussed in this article should not be constituted as investment advice.

Disclosure: We own positions in some/all of the tickers mentioned in this article.